Even before the COVID-19 pandemic, consumers were increasingly turning toward digital banking options, including ATMs, online banking, and mobile banking. Data from the 2017 Federal Deposit Insurance Corp. (FDIC) “National Survey of Unbanked and Underbanked Households” shows that 63.0% of respondents used online banking to access their accounts in the last 12 months, up from 55.1% in 2013, and 40.4% used mobile banking in the past 12 months, up from 23.2% in 2013.

This is comparable to data from the 2017 Federal Reserve Board’s “Survey of Household Economics and Decision-making (SHED),” which estimates that about half of U.S. adults with bank accounts had used a mobile phone to access a bank account in the last year.

Overall, 36.0% of respondents in the 2017 FDIC survey use online banking as the primary method to access a bank account, 15.6% use mobile banking, 19.9% use ATMs or kiosks, and 2.9% use telephone banking versus 24.3% who primarily use a bank teller.

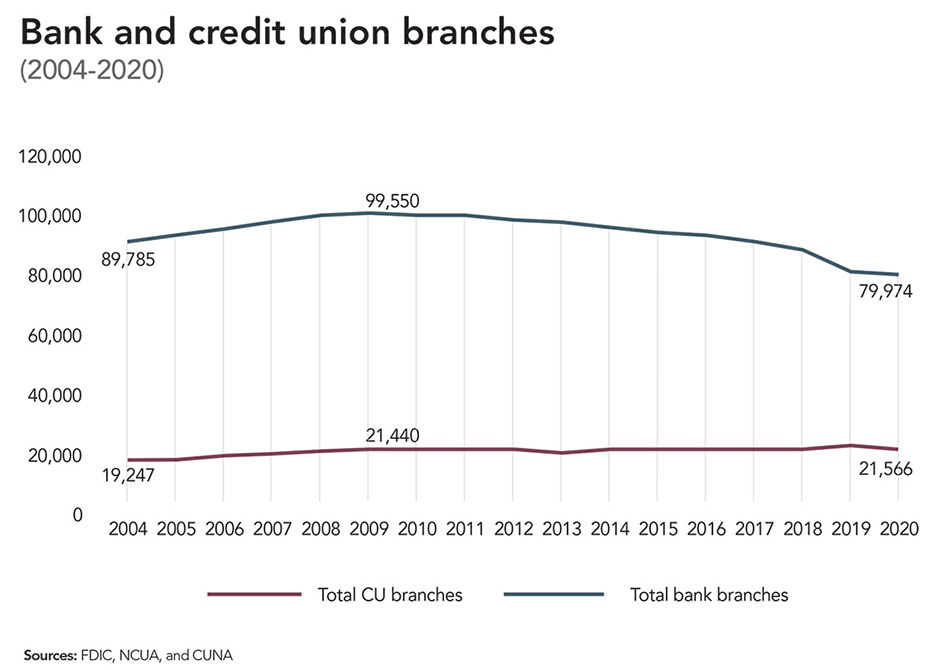

Click to enlarge. Bank and credit union branches.

Credit unions have generally responded to these changing norms: The percentage of credit unions that offer mobile banking services has increased from a small minority (5.7%) in 2009 to a substantial majority (65.2%) in 2019. During that same period, the percentage of credit unions that offer online bill pay and electronic statements grew from 49.6% and 56.3%, respectively, to 67.8% and 72.2%.

As might be expected, banks are even more likely to offer mobile and online banking services. According to a 2016 Federal Reserve Bank of Boston survey, 90% of banks offered mobile banking services.

Moreover, 96% of larger banks and credit unions with more than $1 billion in assets (who serve the vast majority of U.S. households) offered mobile banking services.

Nonetheless, as of the 2017 FDIC survey, most respondents continued to use bank branches: 73.6% visited a teller in the past 12 months, down slightly from 78.8% in 2013. In fact, only 14.0% of respondents did not visit a bank branch in the past 12 months, 30.8% visited one to four times, and 53.6% visited a branch five or more times.

However, these results vary significantly by age, income level, location, ethnicity, and education level. Older, less educated, rural, low-income, and minority populations are significantly more likely to primarily use branches versus mobile and online technologies.

These populations may find it more challenging to access broadband internet, invest in technologies that enable mobile and online banking, and learn new digital banking methods.

For example, in the most recent SHED survey (2019), rural residents were less likely to say they have broadband internet and to have a data plan for a smartphone. Small businesses, seniors, and those lacking consistent and reliable transportation reported being most negatively affected by branch closures.

A 2019 report by the Federal Reserve Board of Governors finds that branches continue to be an important banking channel for consumers—especially for deposit and withdrawal transactions, accessing safety deposit boxes, and for resolving problems—as well as small businesses.

‘While fewer members may enter our doors on any given day, those who do may be the people who most need our help and support.’

Most small businesses prefer to use local banks to access financial services and seem to garner tangible benefits in terms of credit availability and preferable terms. A majority of mortgage borrowers also indicate that the presence of a local branch and an existing relationship with a financial institution are important when selecting a mortgage lender.

Rigorous academic research highlights the continued importance of the branch. “Relationship lending,” in which lenders use “soft information” about borrowers through repeated interactions over time, can enable lenders to make better underwriting decisions.

Various studies demonstrate that loan applicants who are relatively close to their lenders are more likely to be approved for loans and less likely to default.

Proximity and soft information are particularly important for low-income populations. Credit scores and other underwriting techniques based on hard information are likely to be less effective in low-income markets because the quality of the information is lower and the average risk of the potential loan applicant is higher.

One study finds that for low-income borrowers, mortgage originations increase and interest spreads decline when there is a bank branch located in a low- to moderate-income neighborhood.

Branches are also shown to be incredibly important for small business lending, and increased distance between small businesses and branches leads to fewer small business loans and slower economic growth. These findings may, at least in part, explain why surveys and interviews by the Federal Reserve show that small businesses have a strong preference for using branches to access financial services.

Small businesses report significantly higher customer satisfaction levels with small banks and credit unions relative to large banks, online lenders, and finance companies. Also, 61% of small businesses listed “existing relationship with lender” as a reason for applying to a bank, highlighting the importance these institutions place on relationship lending.