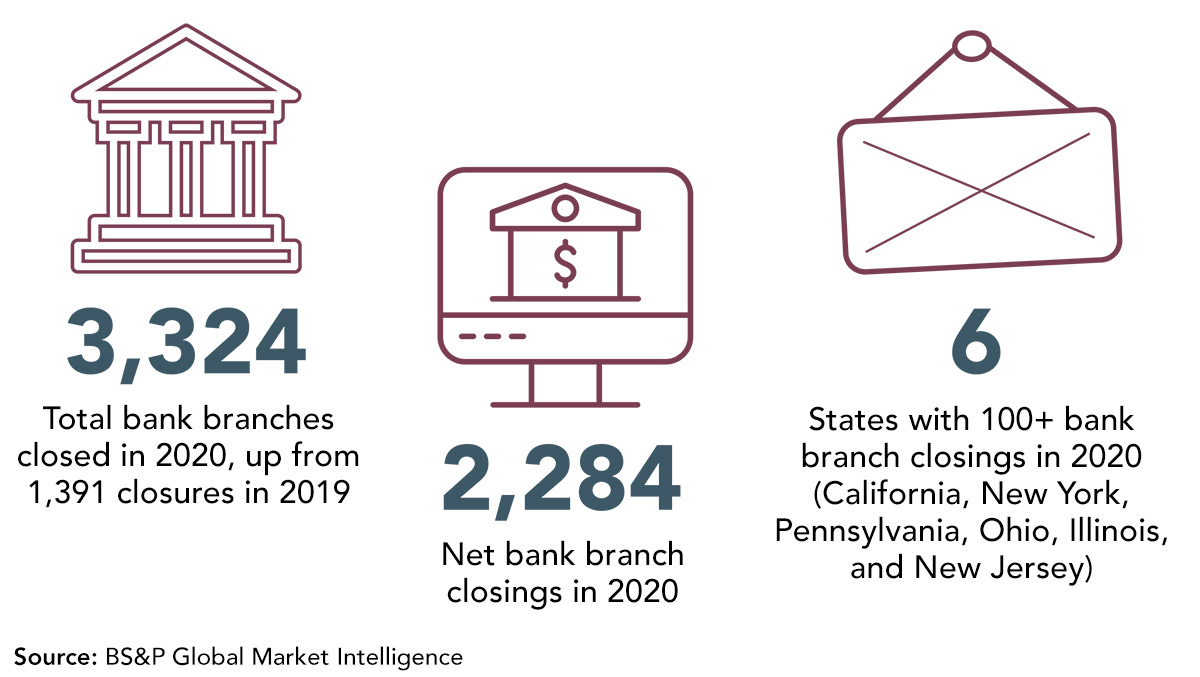

The pandemic and the subsequent rapid transition to digital banking affects not only the number of branches but how customers use them. As credit union members get used to performing routine transactions online or via mobile phones, they become less likely to visit branches.

Those visits are typically for more complex transactions and questions, including loan applications, complaints, financial planning, or trusted financial advice.

This trend has led some to refer to future branch visits as more akin to a doctor’s visit—something you do perhaps once or twice a year and typically for emergencies, complicated questions, or annual check-ups.

For credit unions—who stand out for member service, personal relationships, and financial education—the question of how to use branches in the future is particularly salient and presents both an opportunity and a challenge. Credit unions should resist the urge to simply follow the trend of closing branches to cut costs, even if foot traffic has fallen significantly.

While fewer members may enter our doors on any given day, those who do may be the people who most need our help and support. We could redesign branches to better cater to personal relationships and longer conversations, such as by having more open floor plans, quality coffee and snacks, waiting areas for children, or free Wi-Fi.

Drive-thru services could cater to both quick transactions and longer queries, such as by having designated lanes for quick deposits/withdrawals and those for longer loan applications or financial advice (with the lane requiring the most member interaction closest to the teller window).

Many credit unions have already deployed video kiosks, including in smaller “mini branches,” that allow a conversation and face-to-face interaction with a person without having to be in the same location.

Even before the pandemic, financial institutions experimented with designing branches to be more like cafés or coffee houses. For example, Capital One Cafés offer coffee, food, free Wi-Fi, fee-free ATMs, and iPads that invite customers to take short financial lessons or quizzes to test their money knowledge.

They also include dedicated spaces where people can sit down with financial experts (“Café coaches”) and a touchscreen for money coaching sessions. Credit unions could implement similar ideas that promote personal relationships as well as financial education and financial literacy classes and workshops—high-touch activities that are more difficult to promote via digital channels.

With these changes, credit unions will also need to consider the qualities, attitudes, and skills their frontline employees should possess when making hiring decisions and training staff. For example, floor staff will need to be friendly, welcoming, and empathetic, but also knowledgeable and skillful enough to quickly resolve complaints and solve challenging questions.

Nothing is more frustrating for a member than driving all the way to a branch to speak to someone in person and then not have their problem resolved. And many of these members might have already tried resolving their problem online or by phone without success, and could be particularly irritated.

Members want to feel they can trust their financial provider to listen to them, empathize, have their best interests at heart, and resolve their problems. This is typically best achieved in face-to-face interactions when you can look into the eyes of the person on the other side of the transaction.

Fortunately, credit unions are already rising to the challenges of the pandemic and changing consumer behavior.

CUNA surveys show that around 80% of credit unions have created new loans to meet members’ pressing needs during the pandemic, nearly 95% have offered loan modifications, more than 90% have waived fees, 62% have enhanced drive-thru transactions, 63% offer flexible work schedules for employees, and about half of credit unions have enhanced their mobile app capabilities.

No doubt credit unions will continue to innovate with their branches, too, mindful of both changing consumer preferences and technology adoption, as well the needs of our most vulnerable members and our comparative advantage in member service and relationship banking.