One of the NCUA Board’s primary missions is protecting the safety and soundness of the credit union system. A key focus of this obligation is maintaining a strong and healthy share insurance fund which promotes confidence in the credit union system.

The National Credit Union Share Insurance Fund (NCUSIF) equity ratio (which consists of the fund’s retained earnings plus credit unions’ 1% deposits divided by total insured shares) is the overall capitalization of the insurance fund to protect against unexpected losses from credit union failures.

NCUA is required to charge a premium if the equity ratio falls below 1.20% and is prohibited from charging a premium if the ratio exceeds 1.30%.

The insurance fund’s so-called “normal operating level” (NOL) is the board’s desired equity level for the share insurance fund. In accordance with the Federal Credit Union Act, the NCUA Board sets the normal operating level between 1.20% and 1.50%.

The policy for setting the NOL, adopted in 2017, established a periodic review of the NCUSIF’s equity needs. At least annually, NCUA staff reviews the level at which the NOL is set and reports this information to the board.

Board action is only necessary when it determines a change in the NOL is warranted. The policy establishes that any change to the NOL of more than one basis point shall be made only after a public announcement of the proposed adjustment and opportunity for comment.

Return NOL to 1.30%

In 2017, the NCUA Board increased the NOL to 1.39% because it merged the Temporary Corporate Credit Union Stabilization Fund (TCCUSF) into the NCUSIF. Prior to this, the fund’s NOL had been at 1.30% since 1984, including during the Great Recession, which the board determined did not necessitate an increase.

Much of the 2017 increase to 1.39% was related to legacy asset volatility associated with the corporate credit union resolution. Specifically, that portion of the increase related to the idea that the legacy assets in the corporate credit unions might, from a valuation perspective, fluctuate significantly between 2017 and 2021 or 2022, or whenever the corporate resolution was completely unwound.

The increase was necessary to ensure an adequate buffer in the event those valuations declined substantially.

Another reason the board increased the NOL in 2017 was to ensure it could withstand a modest economic downturn based on modeling using Federal Reserve economic forecasts.

The NCUSIF did suffer a substantial loss during the Great Recession in the wake of the housing crisis. However, that loss did not stem from natural person credit unions.

Instead, it arose from the conservatorship of four large corporate credit unions, each with extremely high concentrations of private label mortgage-backed securities in their portfolios.

Since then, the corporate system has been modified so much as to be almost unrecognizable compared to a decade ago. That change was for the most part driven by the NCUA’s reaction to the crisis.

Corporate credit unions

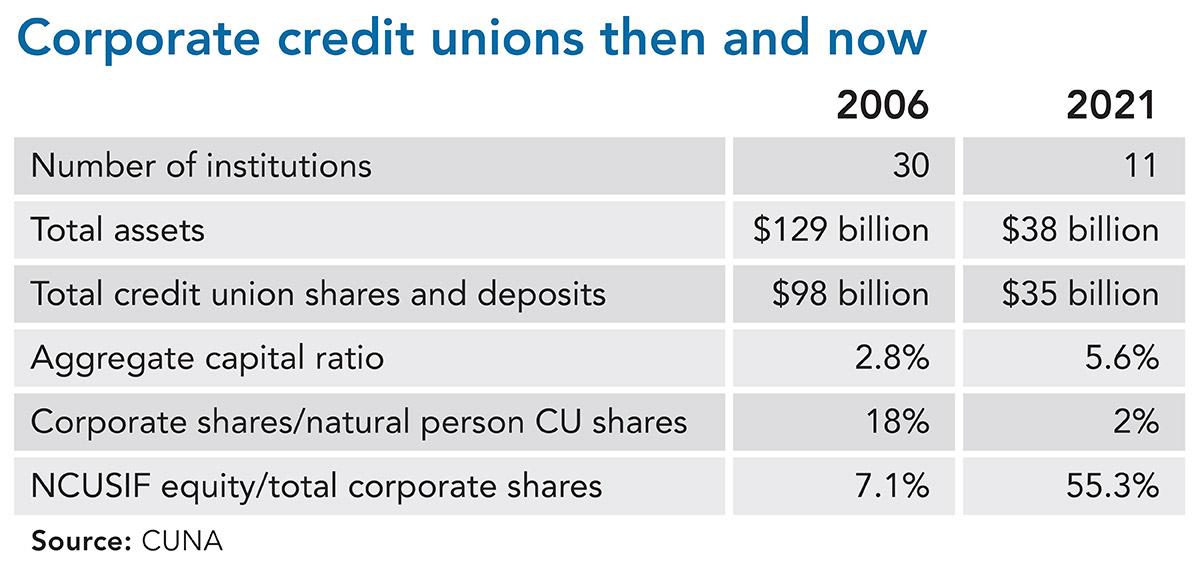

Before the housing/financial crisis at the end of 2006, there were 30 corporate credit unions with total assets of $129 billion and total shares of $98 billion.

Those shares amounted to 18% of the insured shares in all credit unions and the NCUSIF equity was equal to only 7% of total corporate shares. The aggregate capital ratio of the 30 corporates was 2.8%.

After the crisis, NCUA imposed a new, far-reaching corporate credit union rule governing corporates’ operation that included much more stringent investment limitations and higher capital requirements.

As a result, today there are 11 corporates will total assets of just $38 billion and total shares of $35 billion. Those shares now represent just 2% of insured shares in all credit unions.

NCUSIF equity compared to total corporate shares is now more than seven times greater than it was in 2006. The aggregate capital ratio of the 11 corporates is 5.6%—double that reported in 2006.

The corporate credit union system today is healthy and much smaller than it was a decade ago, with total assets at only 29% of their 2006 level. Plus, almost all the potential risk has been regulated out of the system: investment rules are much more restrictive and the average capital ratio is well above 2006 levels.

Thus, the fund experiences during the financial crisis bear no resemblance to the conceivable range of possible experiences in the current reconfigured corporate credit union system.