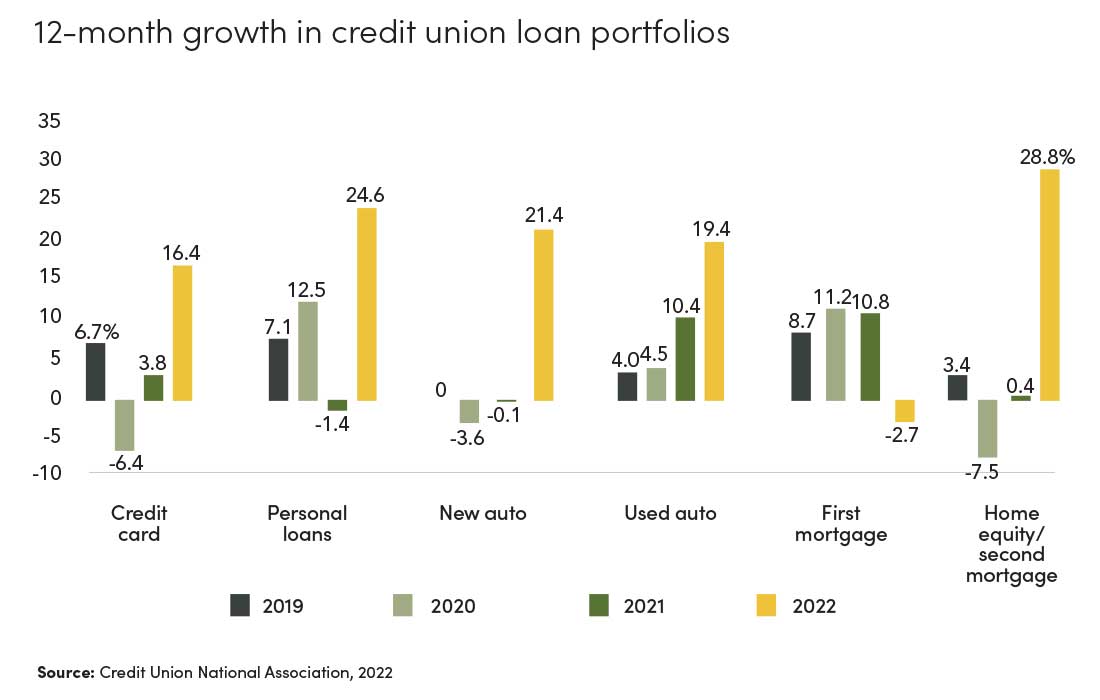

Credit union loan portfolio growth in 2022 was exceptionally strong. CUNA’s Monthly Credit Union Estimates indicates that loans grew 19.4%, a modern-day record annual growth rate which is 2.5 times greater than the average loan growth in the last 10 years.

It also outpaces the 15.3% growth rate observed in 1994.

This unprecedented growth is widespread across all portfolio segments excluding first mortgages. Credit union auto loan balances increased 21.4% and 19.5% for new and used cars, respectively.

Auto loans represent the second-largest portfolio segment for credit unions and account for almost one-third of outstanding balances.

Credit union members across the entire credit score spectrum are more likely to obtain affordable interest rates compared to other lenders, according to analysis of new auto loan origination data using the Equifax analytic data set.

These differences have been more pronounced in the past year as market rates increased. In November, for example, a typical borrower paid an annual percentage rate (APR) of 6.40% at credit unions for a six-year auto loan.

A borrower with the same credit profile paid 7.87% at banks and 8.51% at auto finance companies. The rate difference is even larger for borrowers with nonprime credit scores.

This is critically important: Affordable credit union automobile loans ensure more consumers have access to reliable transportation, which gets kids to daycare or school, and members to work. This significantly reduces the likelihood of income disruptions for millions.

Lower interest rates translate into significant savings in payments over the life of the loan. Deep subprime borrowers—those with credit scores below 580—could save up to $12,000 when they finance a $40,000 auto loan over six years.

Consumers becoming aware of this savings played a role in credit unions being the top auto lenders for two months last year.

The growth in credit card and personal loan balances was also significantly larger than previous years. Credit card balances grew 16.4%, which is higher than the combined 11.5% growth in the past four years.

The 24.5% growth in personal loans in 2022 is nearly equal to the combined 25.1% growth rate registered in the previous four years.

Credit union first mortgage lending declined 2.7% in 2022 due to rising interest rates and changes in the NCUA Call Report data. The average 30-year fixed mortgage rate increased from 3% at the beginning of 2022 to 6% in the second half of the year.

Coupled with high housing prices, this impacted affordability and resulted in a decline of new home loan originations.

New NCUA Call Report data also excludes commercial mortgage loans from first mortgage data, which makes it difficult to compare performance to previous years. Hence, the magnitude of the decline in first mortgages isn’t an apples-to-apples comparison.

On the other hand, home equity/second mortgage loans increased 28.8%. Owners built up a lot of equity as the price of their homes appreciated in the past three years. A significant portion of these owners also refinanced their loans at favorable rates during the pandemic.

Therefore, it’s not surprising that members are tapping into their growing equity.