Cash crop

Credit union innovators boost the learning curve on cannabis banking.

In the fall of 2013, James Collins heard gunshots while relaxing at his home in Central Washington. It turns out a neighbor had an illegal marijuana grow operation, attracting three armed men who showed up at his house.

“They weren’t after his crop; they were after his cash,” recalls Collins, president/CEO at $301 million asset O Bee Credit Union in Tumwater, Wash.

The experience underscores the public safety hazards created with the presence of cash businesses—particularly high-volume cannabis dispensaries.

Serving these types of businesses remains a murky prospect from a legal standpoint, at least on the federal level. Recreational marijuana is now legal in 10 states and the District of Columbia, while medical marijuana is legal in more than 30 states, according to Business Insider.

Because cannabis remains illegal at the federal level, however, it is almost entirely a cash sector. Basic banking services are hard to come by for legitimate businesses, and credit card processing is out of the question.

While some community financial institutions have stepped forward to fill the vacuum, reliable market statistics are elusive for logical reasons.

“There’s a hesitancy for financial institutions getting into this space from putting a target on their backs and jeopardizing relationships with vendors and correspondent banks,” explains Deirdra O’Gorman, founder/president of DX Consulting, which advises financial institutions setting up cannabis programs. “The rule of thumb is, ‘keep quiet.’”

The same holds for cannabis businesses. Once they manage to obtain an account, proprietors don’t want to become too vocal and risk losing the convenience.

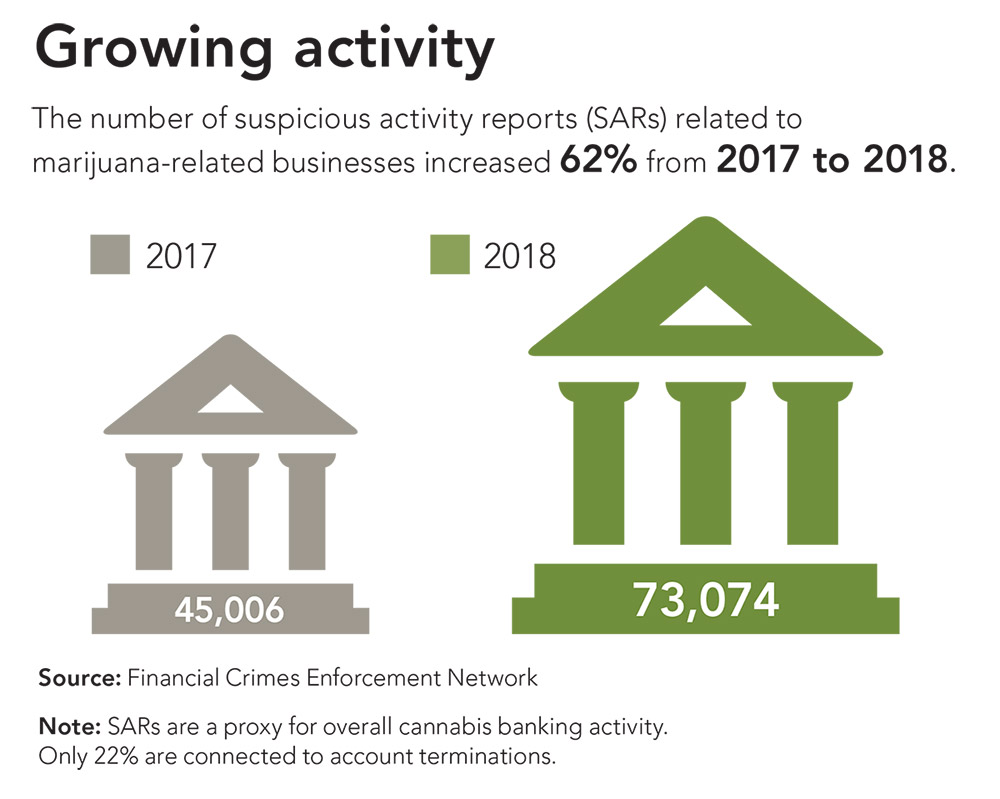

Roughly 30 financial institutions are serving cannabis businesses at scale, but O’Gorman points to an indicator she believes reflects growing activity: Financial institutions filed 62% more cannabis suspicious activity reports (SARs) at the end of 2018 compared with 2017.

According to the Financial Crimes Enforcement Network (FinCEN), 551 financial institutions filed SARs related to cannabis in the fourth quarter of 2018. However, some of this activity could be people filing termination SARs for accounts discovered transacting in cannabis, or financial institutions may be managing only one or two accounts, O’Gorman says.

Here, several credit unions share their experiences as early providers of cannabis-banking services. They shed light on an important issue and prepare other credit unions for the demands of an expanding sector with major implications for public safety, financial inclusion, and credit union economics.

NEXT: Entering the business

Entering the business

O Bee, Maps Credit Union in Salem, Ore., and Numerica Credit Union in Spokane Valley, Wash., entered the field in the latter part of 2014, coinciding with the Justice Department’s issuance of the “Cole Memo.”

This provided a level of comfort that credit unions could operate without undue fear of federal prosecution.

Maps’ entrance into this business came when it found it was already serving some cannabis businesses, says Rachel Pross, chief risk officer for the $745 million asset credit union.

“So, the decision became, whether we shut them down or if we keep them, what is the compelling reason?” she says. “What we got to was the community safety issue, including the fact that these businesses were paying their employees in cash. We have a responsibility to our community, and these businesses are legal in our state, so how can we serve them?

“We took a timeout early on and didn’t accept new accounts until we got scaffolding in place,” she continues, referring to the required regulatory backbone.

“The board vote was not unanimous,” adds Shane Saunders, Maps’ chief experience officer. “There was heated discussion with passion on both sides of the debate. A key factor is that we’re not taking a position on the morality of it.

“The folks we talk to are business people, with growth plans and market strategies,” he continues.

‘No one else was going to step up.’

James Collins

O Bee entered the business when it realized “no one else was going to step up,” Collins says. “We had a member write our board a letter. He ran a sheet-wall business and decided to try something new. We had banked him for some time.

“He said, ‘I’m the same guy, but now that I’m doing cannabis you won’t bank me.’ It made us think,” he continues.

At the time, O Bee had law enforcement on its board, Collins says. “Their attitude was, ‘I’d rather know where the cash is than not, and I’d rather have it here—with cameras.’”

Washington State’s Department of Financial Institutions provided a guiding hand in advance of O Bee’s launch.

“Their attitude was, ‘if you’re going to do this, we’re going to help you do it right,’” Collins says.

Mark Valente takes the same approach as acting commissioner, Division of Financial Services, at the Colorado Department of Regulatory Agencies. The agency regulates state-chartered credit unions in Colorado, the first state to legalize recreational marijuana use.

“The lack of banking and financial services for cannabis-related businesses has resulted in numerous issues, not just for the industry but for the broader community,” he says. “Primarily cash businesses raise public safety concerns, inhibit transparency of the flow of funds to detect nefarious activity, and create challenges for the business to pay its general expenses.

“Allowing financial institutions to provide basic banking services to cannabis-related businesses allows these entities to focus on their business and provides better audit trails for the owners and others to track the funds received,” Valente says.

Once O Bee launched its program for cannabis business owners, Collins discovered another financial inclusion benefit and a welcome, if unexpected, avenue for account growth.

“Employees of these businesses started coming in looking to cash checks,” Collins says. “We discovered that other banks wouldn’t honor a check if they saw the word ‘cannabis’ on it.”

Such prohibitions reportedly remain in place to this day, including one of the nation’s largest banks. “So, we opened accounts for them,” he says.

Financial access issues run even deeper, leading Collins to champion indirect lending to cannabis-industry employees through O Bee’s existing credit union service organization.

‘Our board was very brave.’

Lynn Ciani

“You’re probably not going to get an auto loan if your employment verification shows cannabis,” Collins says. “So, your loan is probably from one of three credit unions.”

“Employees of the industry are being denied services, and they tend to be lower income,” adds O’Gorman. “That’s a story that goes unreported, and I wish more financial institutions would step up.”

Saunders concurs. “I met an entry-level employee manning a booth at a cannabis conference who told me how awesome it was to have direct deposit. In 25 years of banking I’ve never heard some-one say, ‘I’m stoked about direct deposit!’”

One of Numerica’s tenets is to build its communities, says Lynn Ciani, general counsel and chief risk officer for the $2.3 billion asset credit union. “We figured if we could protect members from the crime attendant with a cash-only industry we would be doing just that.

"Our board was very brave,” she adds. “We brought a proposal to them in March [2014]. They had a lot of questions, which we responded to by April, and they approved it.”

NEXT: A $30 million exit plan

A $30 million exit plan

An indication of the degree of community impact—and depth of the issue—came in January 2018 when then-Attorney General Jeff Sessions rescinded the Cole Memo.

The true linchpin, however, was the FinCEN guidance the Department of Treasury issued.

Not knowing whether this would be withdrawn as well, Pross began taking the necessary steps to unwind Maps’ cannabis program based on the exit plan the credit union had built before entering the business.

This included ordering $30 million of cash from the Federal Reserve to have on hand should associated accounts need to be liquidated.

Pross also began scheduling time for account holders to visit the branch—with armed escorts—to retrieve those balances in cash. Discontinuation of the program would have released $30 million onto the streets, a figure that has only grown since.

Fortunately, the situation proved to be merely a drill. FinCEN stood by its existing guidance and the U.S. attorney with jurisdiction for Oregon, which now has prosecutorial discretion over pursuit of area financial institutions, issued a memorandum regarding his priorities on marijuana enforcement.

These aligned with the tenets of the Cole Memo. “It was a great test of our exit strategy,” Pross says.

To date, no U.S. attorney’s office has expressed interest in pursuing action against such institutions. Guy Messick, president of the legal and consulting firm Messick, Lauer & Smith, questions the wisdom of any other stance.

“Preventing these businesses from using financial institutions would create more problems than they’d be solving,” he says.

One lesson learned is the prescribed 24-hour wind-down was not in the best interests of employee or community safety. Numerica’s contingency plan contemplates a month-long process, during which Ciani and her team would line up appointments with affected account holders and determine the best method of funds remittance.

A trend toward legalization

Click to enlarge.

With the Cole Memo in the rear-view mirror and a clear trend toward legalization in states across all geographies, more credit unions are quietly exploring opportunities. An anecdotal metric is the number of requests these early movers are fielding for informational sessions.

O’Gorman estimates “30 to 40 states” have reached out to her firm for additional information, and between them, Pross and Ciani have spoken with credit union groups in Florida, Oklahoma, Michigan, Massachusetts, and throughout the Midwest.

“Once Treasury announced they’d stand behind the FinCEN guidance and no U.S. attorneys pursued action, a lot of the shock effect wore off,” Messick says.

The fact remains that cannabis is illegal under federal law, however, and a shift in enforcement policy is hardly implausible.

The first traction to address this conundrum on a federal level came earlier this year, when the CUNA-backed Secure and Fair Enforcement (SAFE) Act was the first to receive a hearing in the new Congress following the government shutdown.

The SAFE Act would provide financial institutions with a safe harbor in states where cannabis has been legalized—with the key requirement that the state regulator has authorized and implemented a compliance structure.

Rep. Ed Perlmutter, D-Colo., who has a unique vantage point on the issue’s impact on his state, has championed the legislation.

The timing of the hearings is “a testament to how strongly Rep. Perlmutter has been advocating this point,” says Jeremy Empol, vice president for government affairs at the California and Nevada Credit Union Leagues.

Pross testified at the five-hour hearing, which is available for viewing.

“If you watch the questions, you realize that people—and more so members of Congress—really don’t understand the depth of the problem,” says Empol. “Rachel made a great point that law enforcement relies on financial institutions as partners: a first set of eyes for the Bank Secrecy Act [BSA].”

Without bank accounts, there’s one less access point for law enforcement, he says. “We need to bring the business out of the shadows so law enforcement can figure out if Joe’s Pot Shop is really that or a front for something else.”

Despite SAFE’s passage from committee on a 45-15 bipartisan vote, with more than 150 co-sponsors having signed on in support, “the path to law is not crystal clear,” Empol concedes, with Senate priorities a key hurdle.

“But we’re further along with the bill reported from committee than we’ve ever been before,” he says. “The pressure is building on Congress to do something.”

NEXT: A labor-intensive business

A labor-intensive business

Credit union leadership teams should be under no illusions about the effort that goes into serving cannabis businesses.

“Some people see dollar signs, but many of them haven’t thought through the cost, manpower, and due diligence required for full compliance,” warns Empol.

Pross recommends a ratio of one full-time employee for every 15 accounts in the early stages, when onboarding due diligence is particularly heavy and staff is still building expertise and efficiencies.

Maps also requires “BSA 101” training for new accounts to head off surprises and hiccups.

The good news is these credit unions have priced their services to reflect the additional costs. Maps prices its service to be self-funding with an “appropriate” margin, Pross says.

“Our goal is to provide services to these businesses,” she says. “We have no interest in pricing them out of the market.”

Plus, serving cannabis businesses delivers additional credit union benefits by driving more robust risk and BSA programs.

Pross, a 10-year credit union veteran, joined Maps with a mandate to build out a holistic risk and compliance function. The credit union had less than 40 cannabis-related accounts when she joined; now there are more than 500—and it’s safe to say this wouldn’t be possible without a solid risk and compliance backbone.

“Make sure you have robust anti-money laundering and BSA procedures, following to a T the FinCEN guidance documents,” says Jared Ihrig, CUNA’s chief compliance officer. “Certainly, the examiners are looking at that as they come into shops, recognizing, again, that ‘federal vs. state’ tension.

‘Make sure you have robust anti-money laundering and BSA procedures.’

Jared Ihrig

“We recognize credit unions are trying to serve the needs of their communities in this space,” he continues. “But I do expect this to evolve. It’s nothing to enter into lightly. Go into it with eyes wide open with respect to the regulatory expectations and requirements.”

With so few banks and credit unions in the mix, market share has not been a concern for any of these players to date. Although they are beginning to see a bit more competition, market demand will likely grow rapidly enough for the foreseeable future to alleviate any concerns.

Numerica and Maps have each revamped and reduced their pricing multiple times, reflecting a commitment to share economies of scale with members while maintaining fair margins.

Pross wants to dispel any notion that cannabis can be a panacea for liquidity issues. “It’s a fallacy,” she says.

Maps does not include funds from cannabis accounts in its liquidity strategy because doing so would create exposure should the credit union need to shut down the product line.

All parties agree there are no shortcuts. Credit unions must keep third parties such as armored car services and insurers well-informed to avoid disconnects, Collins says.

O’Gorman raises a warning flag about “companies coming in on the payment side promising credit card solutions by recycling bank identification numbers or routing offshore.”

Even these early movers with robust compliance programs confine their offerings to basic account services for a reason: It’s easy to take a misstep.

“If one credit union makes a mistake,” Pross says, “it’s going to reflect poorly on all of us.”

NEXT: Medical model

A medical model

Despite the locations of these early movers, “I definitely don’t see this as a West Coast issue,” says Pross, who also believes there is potential for a viable financial services business in states that have approved cannabis for medical use only.

VSECU in Montpelier, Vt., is evidence of this opportunity. The state’s legislation legalizing medical marijuana limits the issuance of licenses to five dispensaries.

Some of these businesses approached VSECU for services, prompting a due-diligence process.

“Federal banks wouldn’t touch it, and state-chartered institutions were leery as well,” says Greg Huysman, director of business services and lending at the $780 million asset credit union.

Before proceeding, VSECU consulted closely with Vermont authorities, who wanted to see an established entity facilitate the removal of cash from the streets.

Among the business benefits, VSECU’s enhanced compliance infrastructure positioned the credit union to serve the subsequently legalized hemp and CBD segments. Out of an abundance of caution, VSECU rolls these accounts under the same cannabis framework.

Like O Bee, the credit union has seen an inflow of individual accounts from employees of these companies, who ran into bureaucratic roadblocks elsewhere.

New York state took a similar approach to medical marijuana legalization, issuing a handful of licenses.

SEFCU in Albany, one of the state’s largest credit unions, conducted a “long and deliberate due diligence process” which led to account openings for two of these licensees, says Michael Castellana, president/CEO of the $3.8 billion asset credit union.

As the process neared completion, however, the Federal Reserve Bank of New York expressed reservations, leading SEFCU to reverse course rather than put its Fed account at risk.

SEFCU is now waiting for a federal solution or safe harbor legislation that would allow it to provide banking services to this large and complex industry.

“It’s an easily solved problem, but it begs for a federal solution,” Castellana says.

Even credit unions with no desire to pursue cannabis accounts are likely more involved than they realize.

“In states with both recreational and medical activity, it’s hard to keep those funds out of your institution,” O’Gorman says. “Invariably, there will be an electrician, attorney, or someone else providing services to those licensed businesses whether you like it or not.

“Some financial institutions enter the field because they’ll learn more and have information at their fingertips to intelligently assess the risk,” she continues. “It’s a situation that can’t be sustained,” Messick says. “It has to change.”

Fortunately, the credit union movement has some innovators to boost the learning curve.