Digital assets here to stay

Despite market volatility, strong consumer interest in crypto requires an understanding of this market.

The cryptocurrency market has recently been in crisis mode, with many exchanges reporting massive declines in asset values and significant liquidity challenges. Crypto investors, including credit union members, have racked up hundreds of million dollars in digital losses.

Although the current state of cryptocurrency and digital assets remains uncertain—largely unregulated with minimal financial institution and government involvement along with extreme volatility—the market is here to stay.

On the supply side, Big Tech and fintech firms such as Apple, PayPal, and Venmo continue to provide crypto offerings for consumers. These firms offer innovative solutions, including digital wallets and mobile payment apps that make it easier for consumers to complete crypto transactions with their smartphones.

On the demand side, consumers increasingly prefer digital products, continuing a trend accelerated by the pandemic.

Cryptocurrency matters for credit unions because even in a more regulated, consumer-friendly form, digital assets such as stablecoins and retail digital currencies represent an existential threat to credit unions’ deposit funding.

Widespread adoption of privately issued digital assets will likely threaten the Federal Reserve’s ability to effectively implement monetary policy and will continue to conceal a wide range of unlawful activities.

Digital assets describe the universe of tokenized assets that don’t rely on a central bank or a third-party institution to authenticate their value or their transference, according to The Economist.

Conceptually, there are three types of digital assets, which are often viewed as one because of their technological and functional similarities. But they differ by the nature of the organization of origin from privately issued crypto assets to publicly issued central bank digital currencies (CBDCs). They also present structural and design differences, which makes it vital to consider each individually when evaluating potential use cases and needed regulation.

Cryptocurrencies are characterized as being tokenized and not account-based, and are built on decentralized ledger technologies, such as blockchain. Like physical tokens used in gaming arcades, cryptocurrencies are a form of digital tokens consumers can purchase with traditional currencies and use for specific purposes.

Blockchain is a database that isn’t stored or centralized in a single computer. Its data is distributed across many computer nodes, each with a copy of the entire database. The decentralized nature of blockchains guarantees the fidelity and security of the data without the need for a trusted third-party verifier.

Bitcoin was the first cryptocurrency introduced to the market in 2009 as a peer-to peer payment system. But it hasn’t been widely adopted as a means of payment due to its extremely high price volatility. Instead, it’s mostly used as a speculative asset.

Cryptocurrencies such as bitcoin are classified as commodities under the Commodity Exchange Act. As such, their prices are set by supply and demand.

Stablecoins are cryptocurrencies introduced to address the risks of high price volatility associated with other crypto coins. Stablecoins peg their value to an asset or a group of assets for stability.

Most outstanding stablecoins are pegged to the U.S. dollar, and they are mainly used to facilitate trading, lending, or borrowing of other digital assets through digital trading platforms.

CBDCs are digital assets issued by a central bank as a digital form of fiat money. Like cryptocurrency and stablecoins, CBDCs are tokenized and can be exchanged in a decentralized manner.

CBDCs are divided into wholesale or retail assets. A wholesale CBDC is a central bank-issued digital token intended to be used by financial institutions for cross-border and interbank payments. Consumers use retail CBDCs for retail transactions.

Crypto proponents say cryptocurrencies, and digital assets in general, have multiple advantages compared to traditional payment vehicles:

- Crypto transactions are easier to make as they require only a smartphone app.

- The security of crypto transactions is said to be guaranteed by encryption and by the decentralized nature of blockchains.

- Crypto users can set up digital platform accounts in anonymity for an extra level of privacy.

Widespread adoption of digital currencies in their current iteration would pose risks to consumers, financial intermediaries, and governments, including central banks. Speculative trading in digital assets presents market integrity risks such as fraud, market manipulation, insider trading, and front running.

The increasing adoption of stablecoins or retail CBDCs risks disintermediation of financial institutions, including credit unions. An extreme scenario in which we see significant consumer adoption of digital assets as their primary store of value or medium of exchange could disincentivize consumers from holding their savings in depository institutions. As a result, credit unions could see a significant reduction in their source of funding.

Digital currency platforms also offer products and services outside the scope of regulation, which leaves consumers unprotected and exposes credit unions to unfair competition through regulatory arbitrage.

Widespread adoption of private cryptocurrencies and stablecoins would challenge the Federal Reserve’s control of the monetary base. That means the central bank would not be able to effectively use monetary policy to impact real economic outcomes.

NEXT: Cryptocurrency market

Cryptocurrency market

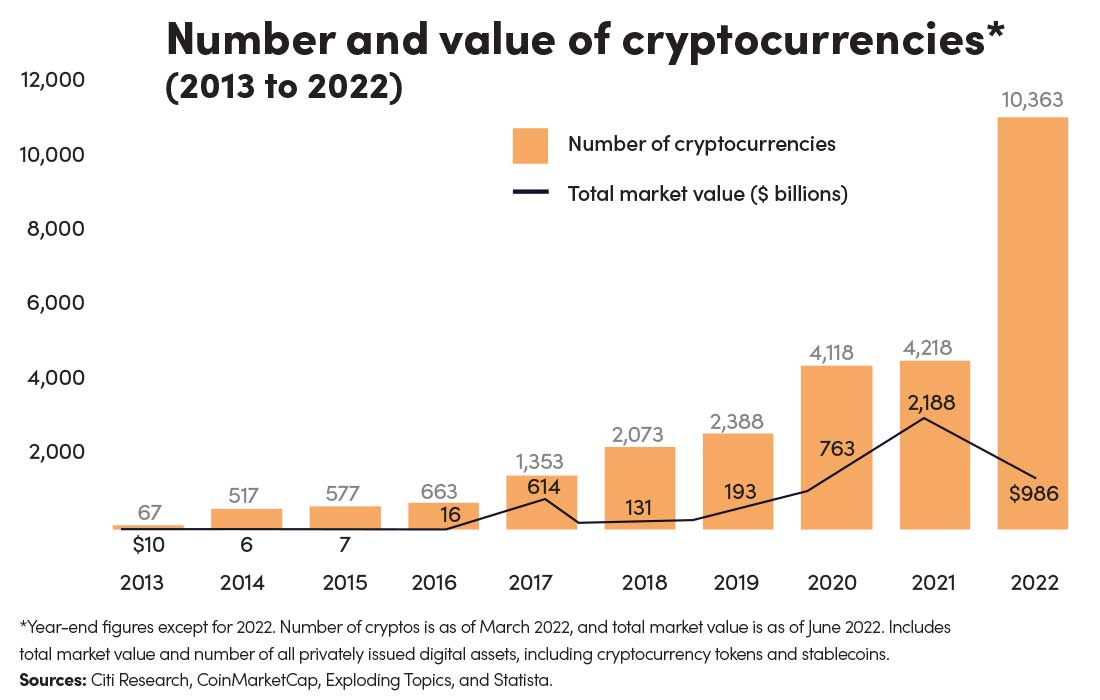

Although the digital asset market size has increased exponentially over the past 10 years, the market value of cryptos has fluctuated widely recently. Since the introduction of bitcoin, the number of cryptocurrencies available in the market has exploded.

Currently there are more than 10,000 active cryptos. After a pandemic-induced market expansion with total market value increasing threefold to $2.2 trillion in 2021 from $763 billion in 2020, the market has plummeted to a current value of $986 billion, a 55% decline (“Number and value of cryptocurrencies”).

A major credit and liquidity crisis recently began, with the value of bitcoin and other cryptocurrencies suddenly plunging. Two major cryptocurrency platforms, Celsius Network and Binance, restricted withdrawals, crypto swaps, and account transfers.

The value of bitcoin and ethereum, the two most highly valued cryptocurrencies, plummeted to their lowest levels in three years with respective value losses of 66% and 75% from their all-time-high prices. Stablecoins such as tether broke its peg to the U.S. dollar, and terra and luna have unraveled with luna’s token price falling from $116 in April 2022 to essentially zero.

This cycle bust has resulted in 46,000 consumers reporting collective losses of at least $1 billion in crypto since January 2021.

As evidenced by current market conditions, cryptos remain subject to extreme price volatility and uncertainty. It’s not surprising that cryptos have not been widely adopted as a means of payment in the U.S.

The total market value of cryptocurrencies in 2020 was less than 1% of the value of transactions paid with credit and with debit cards.

Consumer interest

Rising consumer acceptance for digital finance has been underway for the past decade. In the U.S., cash use has fallen from 40% of transactions in 2012 to 19% in 2020, a trend accelerated by the pandemic.

The CUNA 2022 Voter Survey reveals that most Americans (76%) have used online banking to pay a bill, check account balances, and obtain transaction information. The survey also gauged the extent to which use of crypto aligns with consumer trends toward noncash payments or online finance.

The CUNA survey is conducted on a sample of registered voters, who have higher educational attainment and income than unregistered voters.

Twenty-six percent of CUNA 2022 Voter Survey respondents own cryptocurrency, indicating cryptocurrency adoption is still in the early stage and significantly immature compared with consumers’ adoption of digital finance or other forms of noncash payment.

Plus, a higher proportion of credit union members own cryptocurrencies than nonmembers: 39% of credit union members own crypto compared with 17% of nonmembers.

Despite a relatively low penetration of crypto, survey responses show significant differences in consumer appetite for crypto by age, population density, and race/ethnicity. Younger consumers are the most likely to own cryptocurrency: 59% of members ages 18 to 34 own crypto, compared to 47% of those ages 35 to 64, and 3% of members ages 65 and older.

Differences also exist among racial groups. Forty-eight percent of Hispanic members own crypto, followed by African Americans (34%), Asians (25%), and whites (22%).

The higher propensity of Hispanic Americans to own crypto might be explained by the fact that cryptocurrency is more widely adopted in certain Latin American countries to hedge against inflation and exchange rate volatility. Also, Hispanic Americans might use cryptocurrency to send remittances more efficiently and affordably to their countries of origin.

When asked why they own crypto, 49% of consumers do so as an investment, 29% use it to make purchases, and less than 25% of consumers own crypto for both. However, credit union members are three times more likely than nonmembers to use crypto to make payments (39% vs. 13%).

Nearly one-third (32%) of men own cryptocurrency versus 17% of women.

Research from Cornerstone Advisors indicates 25% of credit unions plan to provide access to cryptocurrency investing and trading by the end of 2023 or later.

Crypto capabilities are something members, especially younger generations, will demand from their financial service provider. If credit unions don’t provide these capabilities, these members may go elsewhere.

Credit unions must build out their financial counseling resources for members around crypto and educate members about the risks and opportunities.

LIGIA VADO is a senior economist at Credit Union National Association. Contact her at 608-609-0678 or at lvado@cuna.coop.

This article appeared in the Fall 2022 issue of Credit Union Magazine. Subscribe here.