‘Every member is a lobbyist’

The CUNA-League team’s fierce, bold advocacy plan highlights those who benefit most from credit unions: members.

While an evenly divided Congress may cause some whiplash due to competing Republican and Democratic priorities, the CUNA-League advocacy team is poised for continued success in 2023, says Jason Stverak, CUNA’s deputy chief advocacy officer.

That’s because both parties embrace credit unions and how they improve constituents’ financial well-being. “Every member can tell the story of how their credit union improves their financial well-being on a daily basis,” he says.

Stverak highlights advocacy accomplishments and surprises from 2022, details priorities for 2023, and explains what success will look like at year’s end.

Credit Union Magazine: The Hill recently named you a top lobbyist. What’s your secret sauce?

Jason Stverak: It’s a team effort. That’s the secret sauce. We have one of the best advocacy teams in Washington, D.C. That includes the incredible people at our Leagues and credit unions who are doing fantastic work on behalf of their members and communities.

Q: What were some advocacy highlights from 2022?

A: I’m happy we were able to pass and get signed into law the member expulsion bill, which will give credit unions additional authority to expel members for specific reasons.

And after being told we wouldn’t get it out of the House, the House of Representatives passed the largest charter modernization in field of membership in over a decade. While it’s stalled in the Senate, we’ve moved that discussion forward.

That’s important, as advocacy isn’t limited by the two years Congress is in session. It’s a continual, 365 days a year, year after year education of current members, new members, old staff, and new staff on issues they should support.

‘We have a simple motto: Trust credit unions to serve their members.’

Jason Stverak

Much of our efforts were geared toward stamping out bad ideas. CUNA has been at the forefront in leading the fight against the Marshall-Durbin interchange bill and has led efforts to protect the entire financial services industry on the overdraft protection issue.

We have a simple motto: Trust credit unions to serve their members. As member-owned institutions, they know what’s best for members, and they’ve done a fantastic job of serving members for many years.

Q: What were some surprises from 2022?

A: Not much of a surprise, but the partisan gridlock and inability of Republicans and Democrats to work together on bipartisan and widely supported issues and pieces of legislation. It’s like they can’t agree the sky is blue some days.

One of the big surprises is that some credit union priorities advanced far without even minor changes. There’s the Credit Union Board Modernization Act, which House Financial Services Committee

Chairwoman Maxine Waters, D-Calif., and ranking member Patrick McHenry, R-N.C., signed off on. It’s not easy getting those two to agree on an issue. But this bill unanimously passed committee and out of the House with 109 co-sponsors.

It’s gratifying to see the acceptance of credit unions’ importance. A few years ago, policymakers would look for money at the end of the year and we’d have to defend our tax status. But that’s not even on the table anymore. It’s not a fight they want to have.

Now we’re at the table looking at and crafting legislation. That’s an incredible advocacy win that will pay dividends into the future. Credit unions are an equal partner at the table because of the hard work we did in 2022.

NEXT: Advocacy priorities

Q: How will CUNA-League advocacy priorities evolve this year?

A: I’ll borrow a phrase from CUNA President/CEO Jim Nussle, who says the issues we advocate for may not change but how we do this must change because of how people communicate. If you go back 30 years, we didn’t have Twitter, Facebook, or other social media, and we didn’t have video. The hot new technology was the fax machine.

How are we reaching out to and educating the next generation of people who are joining credit unions? We also need to educate members of Congress and other elected officials that a strong and vibrant credit union movement is important to the U.S. economy and to their communities.

Plus, we have to take part in advocacy on the regulatory side. Many of the rules or concerns we need to address don’t come from new laws being passed, they’re from regulators. Whether it’s the Consumer Financial Protection Bureau [CFPB], NCUA, or state regulators, we must be aggressive in terms of outreach and education to ensure decisions made on the regulatory side don’t harm credit unions.

Litigation advocacy also is important to roll back or oppose bad rules and regulations, and support those that help credit unions serve their members.

Our advocacy must be fierce and bold 365 days a year. We’re always on offense because that gives credit unions the tools, rules, and ability to serve their members and communities.

That’s where being member-owned is a competitive advantage. Every member is a lobbyist. Every member can tell the story of how their credit union improves their financial well-being on a daily basis. Credit unions help them get their first home, set up their first checking account, or get their first business loan.

Credit unions are the first to raise their hands in traditionally underserved areas of the country that have been overlooked by the banking system and say, “these are the people we’re going to serve.”

That’s a great message we can share as lobbyists and advocates. But it’s infinitely more impactful when that story comes from someone who’s benefited from joining a credit union and asking, “how can I take my first step on the path to financial well-being?”

Q: In what new ways will you share how credit unions foster financial well-being for all?

A: The ability to marry storytelling with data is incredibly important. We don’t get to pick how people get their information, whether it’s Facebook, Twitter, talk radio, or the daily paper.

We take advantage of every communication channel to share the credit union message and ensure people know they should support credit unions. It’s as simple as that.

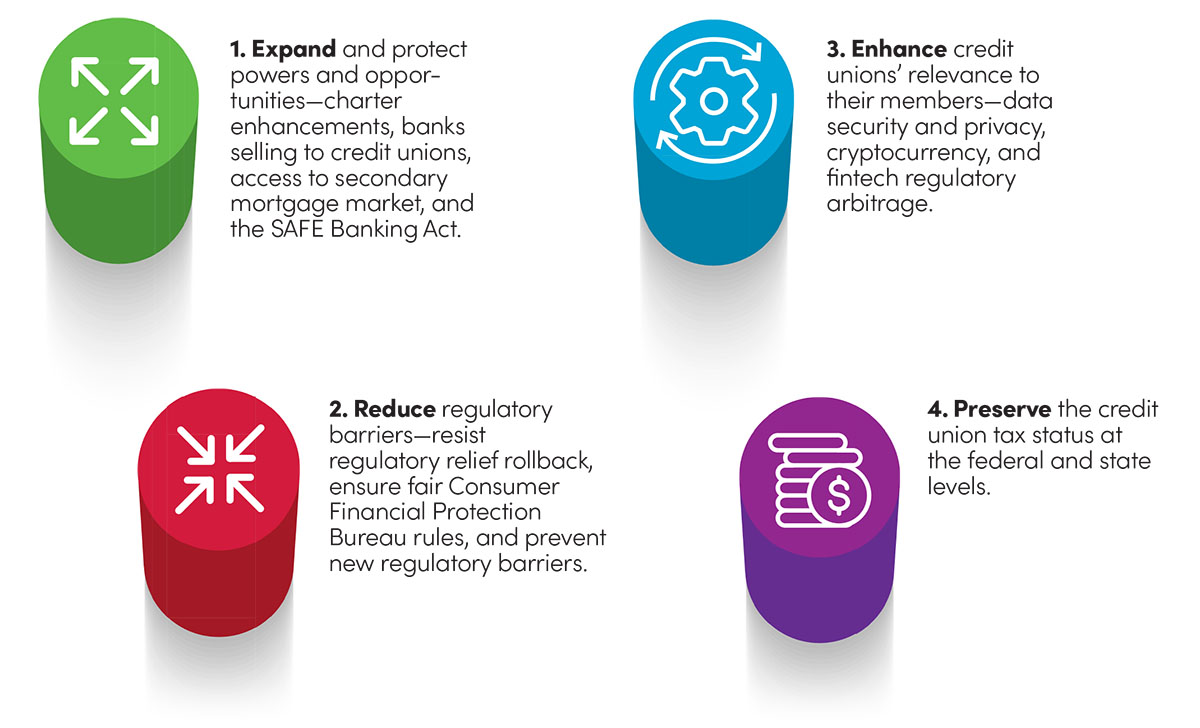

4 pillars of advocacy

Q: What are some threats to credit union interests in the year ahead?

A: Many are threats to noninterest revenue: the continual assault on interchange and overdraft protection. That’s not going to change, especially when you have a CFPB director who gives speeches about junk fees.

Members need to know that, when they’re at the grocery store and they’re short by $5, they can still make that payment, take their groceries home, and feed their family.

That’s a threat we’ll continually talk about to educate members of Congress that they shouldn’t support changes in these areas. We’ll also address data security and privacy.

Q: What will success look like at the end of 2023?

A: Success will be that we’ve advanced the credit union message, had no bill introduced to take away our tax status, and that hundreds of representatives and dozens of senators don’t sign onto overdraft protection legislation that will likely be introduced.

We’re moving forward on our loan maturity rates issue. We had a bill in the last Congress with Sen. Cortez Master, D-Nev., and Sen. Tim Scott, R-S.C.

We’d like to get a markup on raising or eliminating the member business loan cap so credit unions can serve small businesses. There may be an economic downturn or recession in 2023, and small businesses will need additional capital. This will allow us to serve those members to keep the economy growing and moving forward.

There might be a little whiplash going on with an evenly divided Congress. We need to identify common sense, bipartisan pieces of legislation that will pass, and this is where I’m excited on the advocacy side. Whether it’s board modernization, SAFE banking, or the extension of Central Liquidity Facility enhancements, there will be opportunities for us to advance our agenda.

We’re as welcome in former Speaker Nancy Pelosi’s office as we will be in Speaker Kevin McCarthy’s office due to the years of trust we’ve built up with both Democrats and Republicans. That’s because we work on behalf of their constituents to improve financial well-being for all in their districts.