Proving our difference

CUNA economists continue to measure and socialize the transformative power of member-owned credit unions.

The CUNA research and policy analysis team had a busy 2022. We were firmly focused on collecting and using data to bring your stories to life and highlight the credit union difference at the national level.

We spent much of the year on offense, illustrating how credit unions advance the communities they serve and provide true financial inclusion.

As part of that work, we geocoded financial institution branches and mapped underbanked and unbanked communities nationwide to support efforts to broaden credit unions’ fields of membership (FOM) and business lending. We fended off threats to overdraft protection and interchange, and fought to ensure bank owners maintain their ability to sell their institutions to member-owned credit unions, updating our comprehensive white paper on this topic.

Our team championed the expansion of credit union public deposit authority and prepared detailed, customized reports for several state Leagues, which clearly show that a credit union option for financial services is good public policy.

Increasing choice in the marketplace improves convenience, provides greater competition, and strengthens at-risk communities by ensuring community financial institutions lend local funds locally.

The end result is improved service satisfaction and higher returns on deposited funds for trustees of the public’s money.

We assisted with national research on this topic and explored credit union mortgage lending trends in Home Mortgage Disclosure Act data.

We also prepared national- and state-level analyses for several League partners to guard against misguided attempts to expand Community Reinvestment Act provisions into the credit union arena.

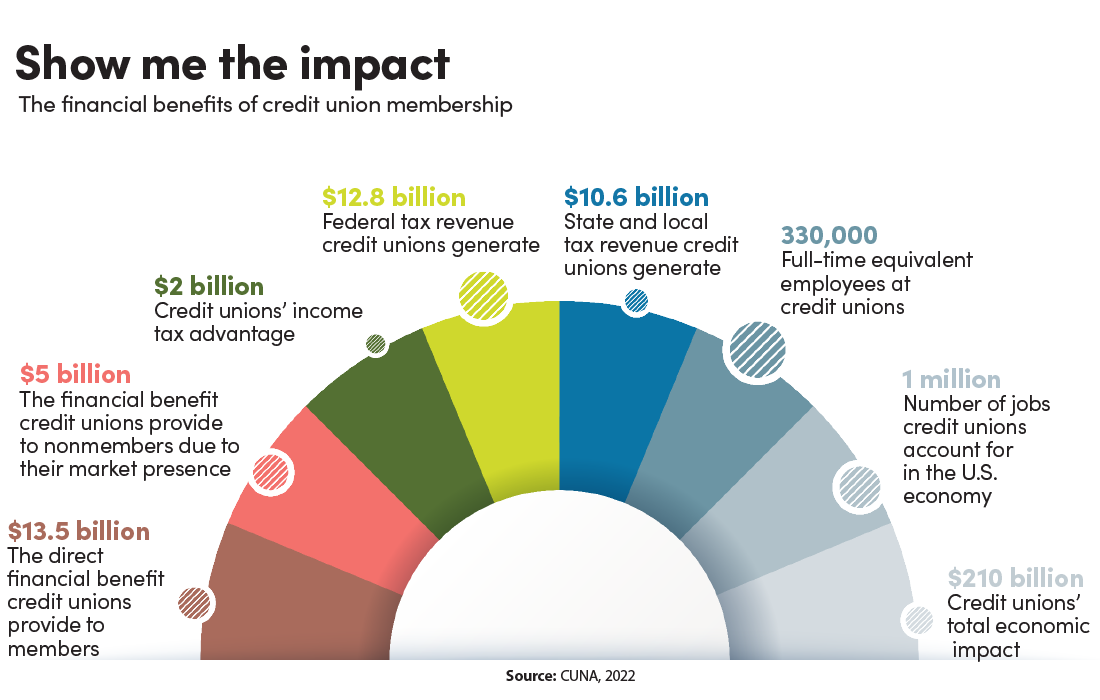

More broadly, we continued efforts to measure and socialize the financial benefits of credit union membership, which totaled $13.5 billion in direct financial benefits to members and more than $5 billion to nonmembers in the 12 months ending June 2022.

This means credit unions collectively leveraged their $2 billion income tax advantage by a factor of more than nine—making this one of the best investments policymakers convey to average Americans.

We also measured our national economic impact, which shows credit unions provide full-time employment for roughly 330,000 people and account for 1 million jobs within the U.S. economy. Collectively, credit unions generate nearly $210 billion in economic output.

They also contribute $12.8 billion in federal tax revenues and $10.6 billion in state and local tax revenues. Beyond this, credit union members paid $1.8 trillion in state and federal income taxes in the most recent tax year.

CUNA Senior Economist Ligia Vado summarized the financial benefits and economic impact in a series of web-based, interactive dashboards that will soon be available to all credit union advocates. Users will be able to drill down from the national data to explore state and congressional district-level data.

Analyzing Equifax data

We also obtained a 10% sample of historical Equifax data, with more than 28 billion records. Senior Economist Dawit Kebede took the lead in organizing, cleaning, and exploring this data.

His analysis shows that credit unions are consumers’ best choice for financing automobile loans.

Specifically, his work shows credit unions:

- Punch above their weight with a whopping 30% auto loan market share.

- Have a consistent mission focus, which is reflected in a subprime share of total originations that’s 1.5 times higher than the share banks report.

- Price in more consumer-friendly ways, resulting in thousands of dollars in lower interest payments for individual borrowers.

- Reflect more resilient borrowers with fewer financial disruptions, including substantially lower 60-day delinquency rates than consumers who use banks or finance companies.

Kebede developed a comprehensive, exploratory dashboard and introduced a monthly credit union auto lending review, which will serve as a springboard for a regular cadence of interactions with both the trade and popular press. The dashboard is coordinated with state-level data that allows League partners and member credit unions to leverage their own information and messaging within their unique fields of membership.

Kebede also harnessed Equifax data to more accurately estimate where credit union members reside, making analysis at county, congressional district, and other political subdivision levels more reliable. He does this by distributing the NCUA Call Report’s 130 million memberships geographically based on the Equifax distribution of member borrowers.

NCUA aggregates call report membership totals at the credit union headquarters level, so each institution’s total membership appears in only one state. The Equifax data allows us to distribute millions of members from large, multistate credit unions to the states where members actually reside.

NEXT: Member relationships

Member relationships

While becoming familiar with the Equifax data, we used CUNA’s annual voter survey to explore how members interact with their credit unions. A white paper summarizing the results shows members are two times more likely than nonmembers to report they have received personalized financial education and/or counseling services at their credit union.

Those interactions are among the top drivers of consumer financial resilience. That’s true in part because a deeper understanding of good financial habits leads to action.

Responses show that members are substantially more likely than nonmembers to establish a financial buffer to shield them during tough times. In fact, nonmembers are nearly two times more likely than credit union members to say they haven’t established a modest emergency savings account to meet unexpected expenses.

Not surprisingly, credit union members are 1.5 times more likely than nonmembers to say they’re “very positive” their financial institution has improved their financial well-being.

Polling results detail similar differences across 10 other dimensions related to financial well-being, including trust, service, and community focus. The results are consistent across all demographic groups, including those in the most financially vulnerable populations.

Working with CUNA’s market intelligence team, we conducted a national consumer survey to measure financial well-being. Conducted in May 2022 by Centiment, the survey employed an abbreviated, six-question poll from the Consumer Financial Protection Bureau.

Findings reveal that credit union members reflect a modestly higher level of financial well-being than nonmembers. While the differences are relatively small, they’re statistically significant.

This is consistent with Financial Health Network findings, and it underlines the notion that credit unions should celebrate the difference—but also realize there’s much work to do.

A lack of financial well-being is clearly evident in the population. But credit union members and employees reflect a degree of fragility we shouldn’t overlook.

While we didn’t celebrate it widely (yet), former CUNA economist Jordan van Rijn published four academic research papers in peer-reviewed journals in 2022. These allow us to emphasize that our structure matters, incentives matter, and credit unions’ people helping people philosophy matters.

Against this backdrop it’s not surprising that, based on an independent study of Washington policymakers, Ballast Research recently reported the CUNA-League system is the voice of the financial services industry on Capitol Hill, providing reliable data and research illustrating how policies impact the average person.

For the sixth year in a row, CUNA was named the most influential financial services trade association. Even more impressive, Ballast named the CUNA-League system as the most credible trade association in Washington across all industries.

Data-based proof points are increasingly important in our advocacy work.

Leveraging those proof points with real-world stories around favorable membership outcomes and behaviors has been—and will continue to be—an unbeatable combination.

MIKE SCHENK is chief economist and deputy chief advocacy officer at Credit Union National Association.