What’s in store for lending?

Despite challenges, CUNA economists foresee solid loan growth in 2023.

Financial institutions have extended large sums of credit to consumers since 2020. While the total balance of household credit declined continuously between the start of the Great Recession in 2008 until 2013, debt levels started to gradually increase, returning to 2008 levels around the beginning of 2017.

Balances grew by $1.6 trillion over the following three years before the pandemic-induced recession began. As of September 2022, consumer debt is $2.36 trillion higher than at the end of 2019, according to the Federal Reserve of New York.

Driving this massive increase in loans: low interest rates during and after the pandemic recession, the subsequent fastest economic recovery in history, and increased consumer demand. Today, set against a backdrop of conflicting macroeconomic signals, lenders seem apprehensive as they think about the credit market outlook in 2023.

There are macro risks driven by high inflation, tight monetary policy, and a slowdown in economic activity with some chance of recession. On the upside, a record-low unemployment rate, a buffer of excess consumer savings despite a downward trend, and pent-up demand for some consumer goods and services could provide some respite.

It’s not easy to predict with absolute certainty how these factors play out in the near future.

When people worry about an economic downturn, they’re less likely to take out loans due to uncertainty about their future financial stability. Higher interest rates make it more expensive to borrow, and reduced affordability almost always lowers demand for loans.

On the other hand, a strong labor market can boost loan growth. Employed people with steady incomes are more likely to take out loans.

‘There is optimism for credit union loan growth despite expected tight monetary policy conditions and an economic slowdown.’

Dawit Kebede

The net impact on this year’s credit outlook depends in large part on whether the Federal Reserve will succeed in its attempt at a soft landing—reversing inflation without recession. And if it doesn’t, the timing of when the risks outweigh the upside influences consumer demand for credit.

Some forecasts push the timing of recession toward the end of 2023 or early 2024.

CUNA economists project that a recession, although more likely than not, will be mild without large losses in employment compared to previous downturns. The impact on credit union lending will be slower growth compared to last year but increases converging with long-run trends.

NEXT: Record performance

Record performance

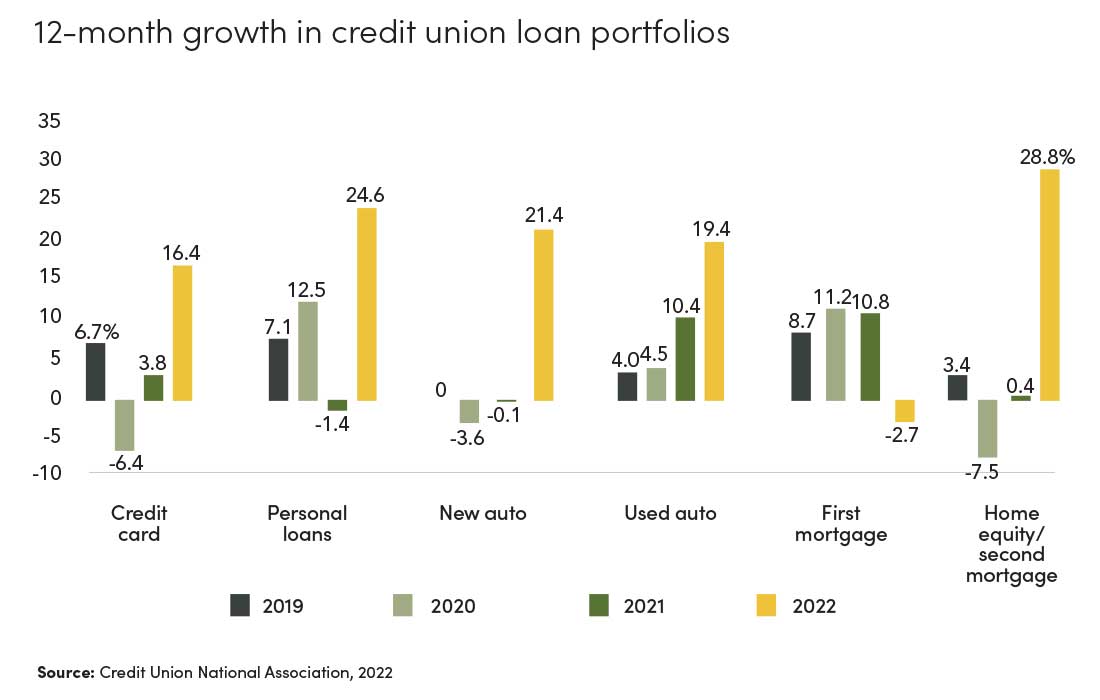

Credit union loan portfolio growth in 2022 was exceptionally strong. CUNA’s Monthly Credit Union Estimates indicates that loans grew 19.4%, a modern-day record annual growth rate which is 2.5 times greater than the average loan growth in the last 10 years.

It also outpaces the 15.3% growth rate observed in 1994.

This unprecedented growth is widespread across all portfolio segments excluding first mortgages. Credit union auto loan balances increased 21.4% and 19.5% for new and used cars, respectively.

Auto loans represent the second-largest portfolio segment for credit unions and account for almost one-third of outstanding balances.

Credit union members across the entire credit score spectrum are more likely to obtain affordable interest rates compared to other lenders, according to analysis of new auto loan origination data using the Equifax analytic data set.

These differences have been more pronounced in the past year as market rates increased. In November, for example, a typical borrower paid an annual percentage rate (APR) of 6.40% at credit unions for a six-year auto loan.

A borrower with the same credit profile paid 7.87% at banks and 8.51% at auto finance companies. The rate difference is even larger for borrowers with nonprime credit scores.

This is critically important: Affordable credit union automobile loans ensure more consumers have access to reliable transportation, which gets kids to daycare or school, and members to work. This significantly reduces the likelihood of income disruptions for millions.

Lower interest rates translate into significant savings in payments over the life of the loan. Deep subprime borrowers—those with credit scores below 580—could save up to $12,000 when they finance a $40,000 auto loan over six years.

Consumers becoming aware of this savings played a role in credit unions being the top auto lenders for two months last year.

The growth in credit card and personal loan balances was also significantly larger than previous years. Credit card balances grew 16.4%, which is higher than the combined 11.5% growth in the past four years.

The 24.5% growth in personal loans in 2022 is nearly equal to the combined 25.1% growth rate registered in the previous four years.

Credit union first mortgage lending declined 2.7% in 2022 due to rising interest rates and changes in the NCUA Call Report data. The average 30-year fixed mortgage rate increased from 3% at the beginning of 2022 to 6% in the second half of the year.

Coupled with high housing prices, this impacted affordability and resulted in a decline of new home loan originations.

New NCUA Call Report data also excludes commercial mortgage loans from first mortgage data, which makes it difficult to compare performance to previous years. Hence, the magnitude of the decline in first mortgages isn’t an apples-to-apples comparison.

On the other hand, home equity/second mortgage loans increased 28.8%. Owners built up a lot of equity as the price of their homes appreciated in the past three years. A significant portion of these owners also refinanced their loans at favorable rates during the pandemic.

Therefore, it’s not surprising that members are tapping into their growing equity.

NEXT: A positive outlook

A positive outlook

Looking forward, there’s optimism for credit union loan growth despite expected tight monetary policy conditions and an economic slowdown. Helpful underlying factors include:

- Growing credit union membership.

- Healthy household balance sheets and favorable debt service ratios.

- Increasingly stable new-auto supply chains.

Total credit union membership as of September 2022 is about 135 million strong. According to CUNA’s Monthly Credit Union Estimates, 2022 saw the fastest growth in membership in more than three decades with an increase of 4.5%.

This follows an increase of 4.3% in 2021. An expanding membership base implies greater potential demand for loans, especially when the unemployment rate is at the lowest level in more than five decades.

Despite the recent increase in total U.S. household debt, debt payments as a percentage of disposable income declined in 2020 and 2021 as people paid down credit card and other debt using excess savings and government transfer payments, and folded higher-rate credit into lower-rate refinanced mortgage loans.

Currently, the percentage of household income that goes to debt payments is 9.8%, which is similar to pre-pandemic levels.

Household balance sheets are strong, with good cash reserves, low delinquency, and a 40-year-low debt burden, according to the Office of the Comptroller of the Currency. Most of the outstanding consumer debt is priced at a fixed rate, which minimizes the risk of rising rates.

Supply chain issues and labor shortages disrupted the auto manufacturing industry and significantly reduced production in 2021 and 2022. Total new vehicle sales prior to the pandemic were 17 million at a seasonally adjusted annual rate. This fell by 4 million units in 2021 and 2022, which drove up prices of both used and new cars.

An increasing supply of automotive chips will improve production this year, according to IHS Markit’s January report. Although rising rates will slow the recovery of vehicle sales, pent-up consumer demand and aging rental fleets will lead to growth of an additional 1 million sales compared to last year, an 8% increase.

Mortgages represent the largest portfolio for credit unions and account for 45% to 50% of outstanding balances at any given time. Fannie Mae expects a cumulative 6.7% home price decline over the next two years. Elevated mortgage rates are expected to limit mortgage originations in 2023, but there’s a projected moderation in the second half of the year.

The Mortgage Bankers Association’s January forecast shows that outstanding balances will increase 3% in 2023 nationally. However, new originations will be lower than last year, and will start to trend up in 2024.

An analysis of mortgage originations since March 2022, when the Federal Reserve stopped the purchase of mortgage-backed securities and began raising federal funds rates, indicates that credit union mortgage pricing is affordable compared to banks and mortgage companies.

Affordable credit union home loans put millions of members on the path to financial security. Homeownership is the top way consumers build wealth. By extension, this also opens the door to significant intergenerational wealth transfers, which builds stronger, more resilient communities.

CUNA calculated the average APR of 30-year fixed mortgage originations using the Equifax analytic data set for borrowers of all credit profiles.

The monthly savings in payment for credit union members ranges from $77 for super prime borrowers to $197 for deep subprime borrowers compared to borrowers with similar profiles at banks and mortgage companies.

This is a significant amount of savings, ranging from $28,000 to $71,000 over the course of 30 years. Consumers are better off obtaining their mortgages at credit unions even when the Federal Reserve is raising short-term interest rates.

Overall, CUNA economists project that credit union loan growth will be 7.5% in 2023, closer to the 10-year average growth rate between 2011 and 2021. This is despite the assumption that the economy will grow below its potential, slowing consumer spending, and the possibility of a mild recession.

DAWIT KEBEDE is a senior economist at Credit Union National Association. Contact him at dkebede@cuna.coop.