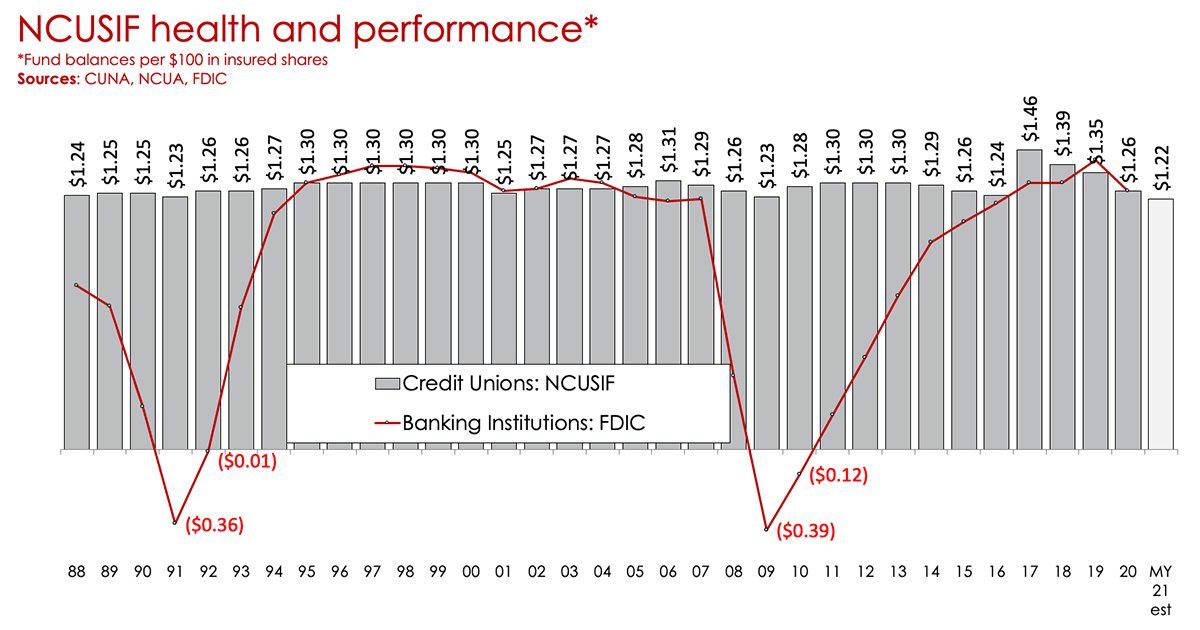

The NCUSIF remains strong. The fund’s pre-pandemic equity ratio stood at 1.35% and finished 2020 at a historically robust 1.26% reading despite massive fiscal stimulus that led to a 20% surge in insured shares during the year.

NCUA projected the equity ratio would fall to 1.22% at mid-year 2021. But the fourth quarter’s 1% deposit true-up, which is based on mid-year insured shares at the nation’s largest credit unions, should mean the fund equity ratio will end the year at 1.25% or modestly higher—even with above-average insured shared growth arising from the expanded child tax credit.

Click to enlarge.

A few small credit unions have failed during the pandemic, but the impact on the insurance fund has not been significant. Also, the number of credit unions with weak CAMEL scores remains unchanged.

While some credit unions serve the commercial real estate, leisure and hospitality, and energy industries, there’s no evidence there will be significant disruption to these industries that would impact the insurance fund.

The continued expansion of the economy and labor market supports this view.

Given the fund’s health and its historically favorable performance, CUNA opposes recent remarks of several NCUA officials, including Chairman Harper, which suggest NCUA may need to charge a NCUSIF premium in the near future and/or that statutory changes to the NCUSIF funding guidelines and NOL are needed.

The Federal Credit Union Act provides that the NCUA Board may assess a premium charge only if the NCUSIF’s equity ratio is less than 1.30% and the premium charge does not exceed the amount necessary to restore the equity ratio to 1.30%. This process has served the NCUSIF and the credit union industry well.

While there is a statutory process in place to ensure the fund is restored if it drops below 1.20%, the agency’s boards over the years have actively managed the NCUSIF to maintain it at healthy levels.

CUNA specifically opposes any legislation that:

Increases the NCUSIF’s capacity by removing the 1.50% statutory ceiling on the NOL.

Removes the interim limitation on assessing premiums when the equity ratio exceeds 1.30%, granting the NCUA Board discretion on the assessment of premiums.

Provides the NCUA Board with the option to use risk-based premiums and total assets as the assessment basis, not insured shares.

As we’ve outlined in recent correspondence with the agency, we believe such proposed changes are truly solutions in search of problems.

Such a drastic, unnecessary approach is inappropriate because there is no apparent problem with the NCUSIF that is begging to be fixed, the historical performance of the NCUSIF relative to the FDIC’s Deposit Insurance Fund is very favorable, and the NCUA Board has at its disposal the tools it needs to properly maintain the NCUSIF.

MIKE SCHENKis chief economist and deputy chief advocacy officer for Credit Union National Association. This article provides an update to a CUNA white paper that addresses the insurance fund.