Piper Sandler Managing Director Jon Searles (left) and Chief Balance Sheet Strategist Scott Hildenbrand.

We’re certain rates are rising, but less certain about the impact to balance sheet management. These discussion points identify key questions in ALCO meetings and reflect the amount of uncertainty facing management teams in this environment.

Liquidity vs. rising rates

As we embark on a rising rate environment, will the historic liquidity in the system help moderate pressure on member shares? Or will the anticipated pace and magnitude of the Fed’s rate hiking efforts force credit unions to keep pace? Data indicates that excess liquidity will overwhelm the hiking cycle, at least initially. Will higher rates lead to outflows? Will there be a migration to higher yielding products now that there is actually an opportunity cost?

Content Sponsored By:

Recent industry trends have reflected a more typical relationship between loans and shares, with growth rates largely aligned. But this comes after share growth outpaced loans by over 20% in the past two years, leading to notably depleted loan-to-share ratios. Given the magnitude of this differential, it is hard to imagine a quick reversion. Additionally, while members decide what to do with their cash, stock market volatility, economic uncertainty, and elevated inflation could lead to maintaining elevated balances in the most flexible products.

Battle of the betas

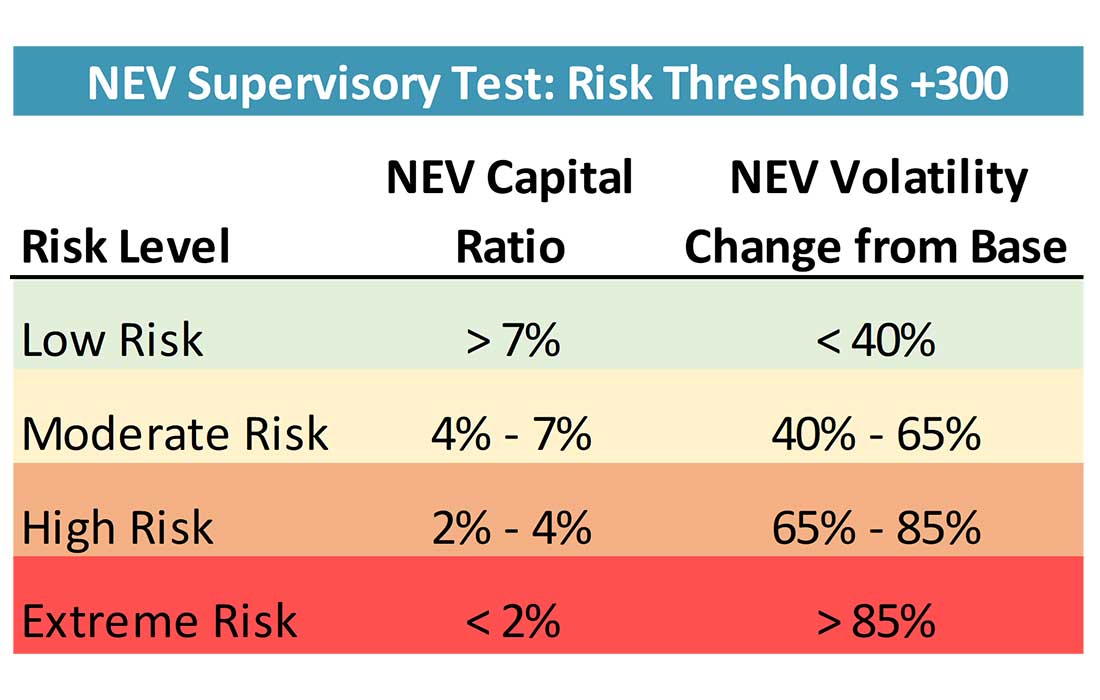

There is a lot attention centered on the industry’s ability to lag share pricing, and we’ll soon be able to differentiate sticky from non-sticky shares. Loan pricing power has thus far been challenged due to excess liquidity and impressively muted credit costs. Bonds have been a different story, as rates have moved higher and spreads have widened for some products, resulting in a dramatic narrowing of the spread differential between bond yields and loan yields. It has been a long time since there was a reasonable debate regarding the risk-adjusted returns between bonds and loans. This comes at a time when bond portfolio managers are licking their wounds from unrealized losses. With net economic value (NEV) and capital limits (shown below), the repricing speed and magnitude will impact capital and volatility risk.

NIM and credit metrics likely both coming off cycle troughs

Will this be a bigger driver to 2022 results and beyond? Excess liquidity and low rates resulted in historically low net interest margin (NIM), while government stimulus and a quick recovery for most borrowers have kept credit costs low. Higher rates are expected to drive both metrics higher, although NIM could get a boost quicker. We’re not necessarily predicting a dramatic downturn in credit, but we are sensitive to what the impact will be to borrowers in a less accommodative environment.

Shift in earnings drivers

Fees benefited from Paycheck Protection Program (PPP) loans and a massive refinance boom with higher home prices. PPP is largely over, and the mortgage market will now have to rely primarily on purchase volumes only. Margin expansion will not be equally distributed across the industry, but if shares can be sticky and asset mixes shift from cash to loans and securities at higher yields, the industry should see higher NIMs. In sum, earnings will likely reflect a tougher fee (and credit) environment and higher non-interest expenses due to inflation, while potential margin expansion could provide some upside.

With margin now a potential key driver for earnings growth, balance sheet management is under heightened focus, particularly around pricing decisions and asset mix. Asset sensitive credit unions are excited to finally benefit from rising rates, but also starting to think about hedging the next rate cycle lower (Is it time to add floors? Or extend asset duration? We recently hosted a webinar discussion on how credit unions are protecting themselves from further exposure and volatility by using interest rate swaps. Reach out for access to the replay).

Liability sensitive credit unions are more focused on today, trying to add floating rate assets and worrying that the cost to add liability duration will be onerous by the time they actually need new funding.