The Federal Reserve has a dual mandate granted by Congress to promote maximum employment and price stability. Traditionally, the primary tool employed to achieve these objectives has been the use of the federal funds rate, also known as the short-term nominal interest rate.

When the economy is weak, the Fed lowers the short-term interest rate to stimulate investing and consumption. It raises this rate when the economy recovers and prices start to rise.

Focus

Quantitative easing during the pandemic stimulated economic growth.

The Federal Reservewill end its quantitative easing program in March 2022, and may raise the federal funds rate three times in 2022.

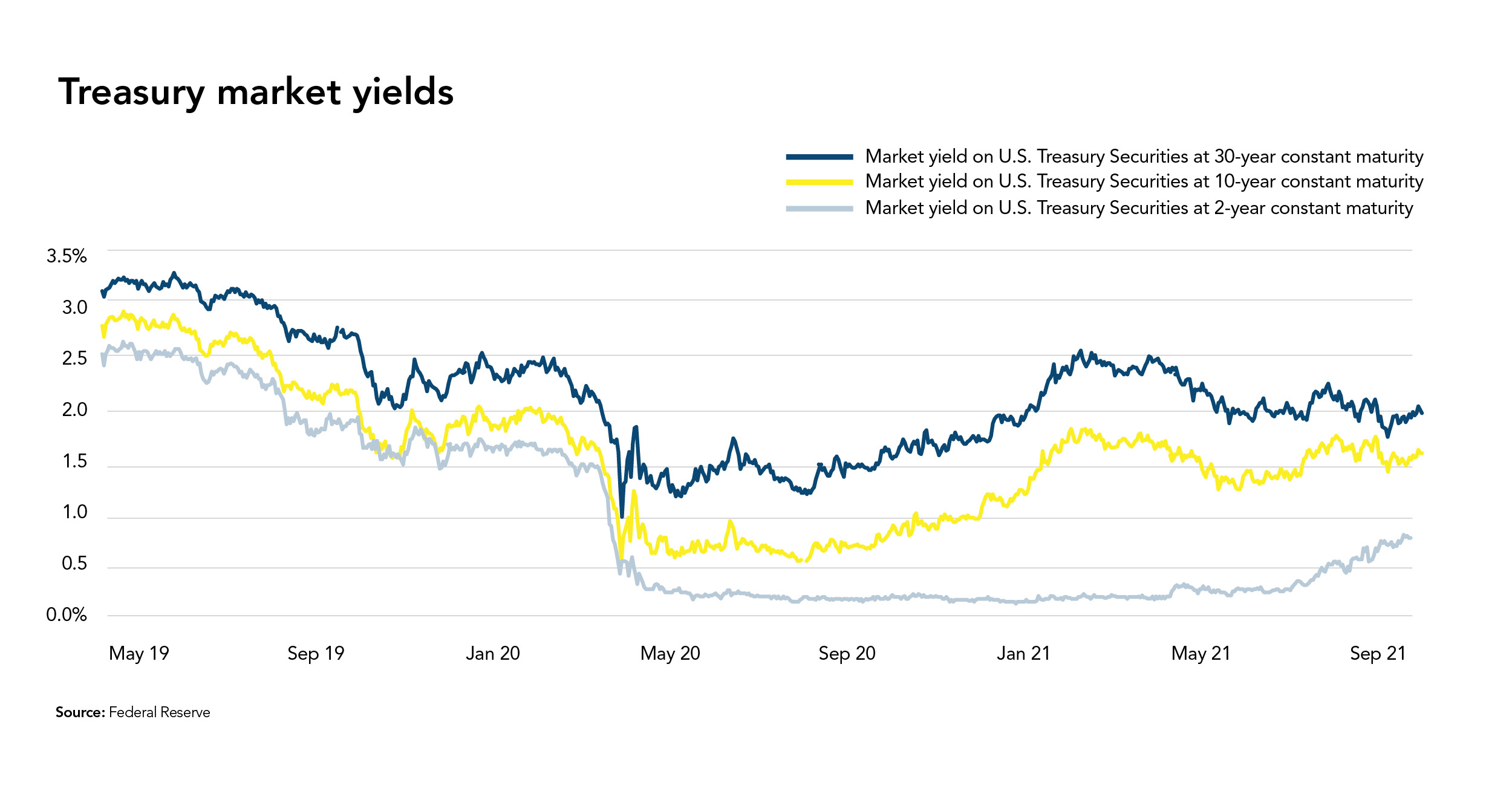

Board focus:The Fed’s decision will result in higher yields on long-term securities and rising borrowing costs for consumers.

The agency conducts monetary policy by buying and selling short-term Treasury securities to maintain its targeted short-term nominal interest rate. When the Fed buys short-term securities it expands the monetary base, which lowers short-term interest rates.

This impacts the prices of different assets, including stocks and exchange rates.

High stock prices lead to more business investment and consumption. Lower exchange rates make U.S. goods more competitive in the international markets, which increases exports. That’s how the Fed uses monetary policy to stimulate the economy.

During the Great Recession, however, this traditional monetary policy was insufficient to turn around the declining economy. The Fed lowered the short-term interest rate close to zero, but the economy was still weak.

Click to enlarge. Treasury market yields

The rate reached the “zero lower bound” and could not go lower. Therefore, the Fed resorted to another tool to stimulate the economy: the purchase of large-scale assets, also known as quantitative easing.

This practice stimulates the economy through its effect on long-term interest rates. It also changes the relative supply of assets available for investors.

Quantitative easing during the pandemic

The coronavirus pandemic caused the largest decline in economic activity since the Great Recession. Second-quarter gross domestic product in 2020 declined at an annualized rate of 33%, and 22 million people lost their jobs in March and April of that year.

The unemployment rate reached a peak of about 15%, consumer spending declined more than 20%, and prices plummeted.

The Fed responded to this crisis by employing the tools it has at its disposal to mitigate the pandemic’s damage to the economy. Among other measures, it cut interest rates, provided forward guidance about its plans for interest rates, and restarted its program of purchasing large-scale assets, specifically Treasury securities and agency mortgage-backed securities (MBS).

First, the Federal Open Market Committee (FOMC) announced it would cut the federal funds rate by one-half of a percentage point on March 3, 2020, to support maximum employment and price stability.

On March 15, 2020, it announced it would further cut rates by one percentage point to zero lower bound, which effectively exhausted its traditional monetary policy response.

It simultaneously introduced forward guidance and indicated it would increase its holding of Treasury and MBS by $500 billion and $200 billion, respectively, in the following months.

The FOMC announced it would purchase $75 billion in Treasury securities and $50 billion in agency MBS each business day during the week of March 23, 2020. It has since made these purchases with varying amounts and frequency.

The FOMC announced it will end this program by the end of March 2022 as inflation soared to a 40-year high.